I believe there are 3 reasons to continue to own $MU: 1) early stage of a cyclical recovery, 2) technology catch-up, and 3) inexpensive play on VR/AR and Self-Driving Car.

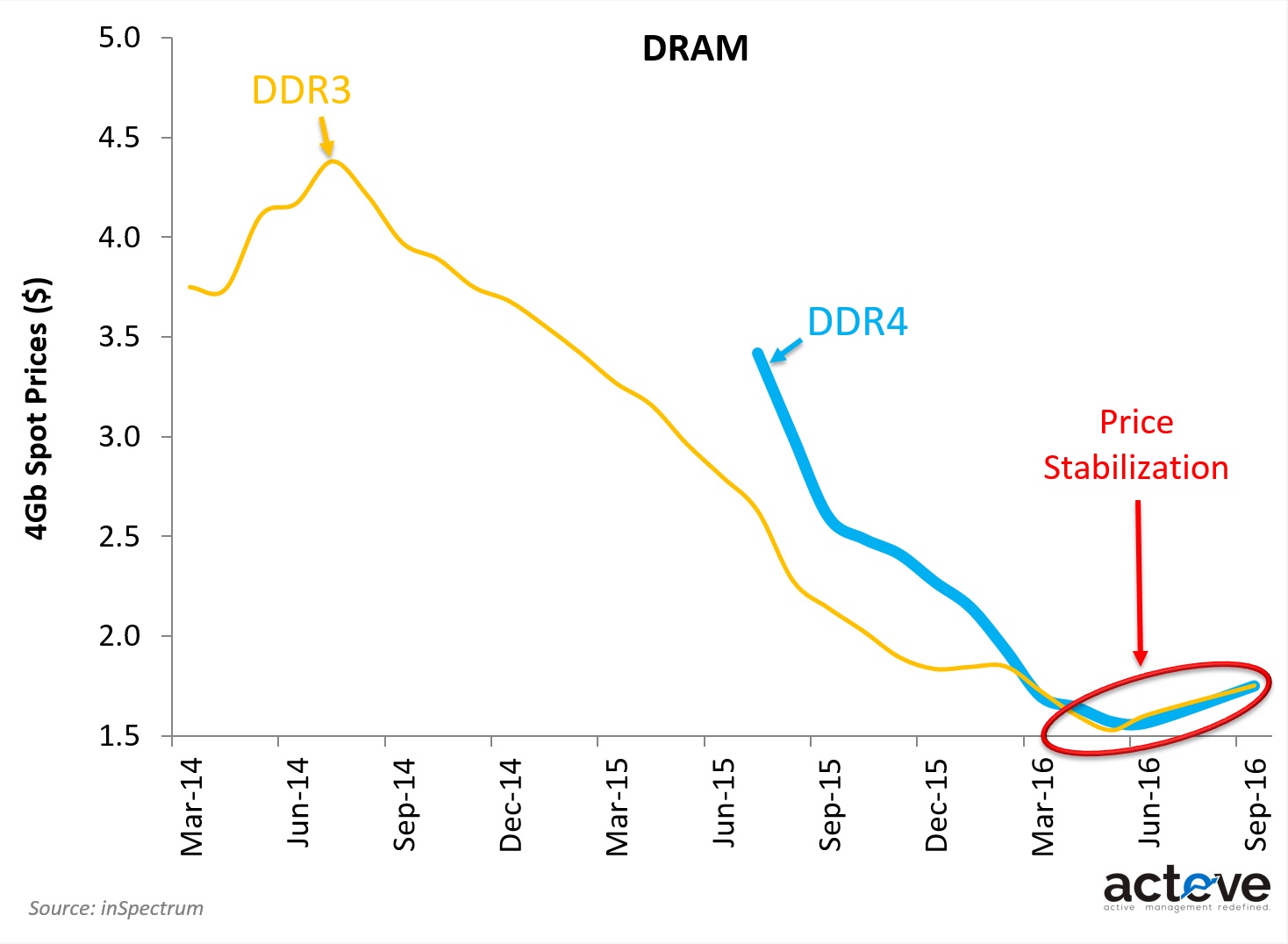

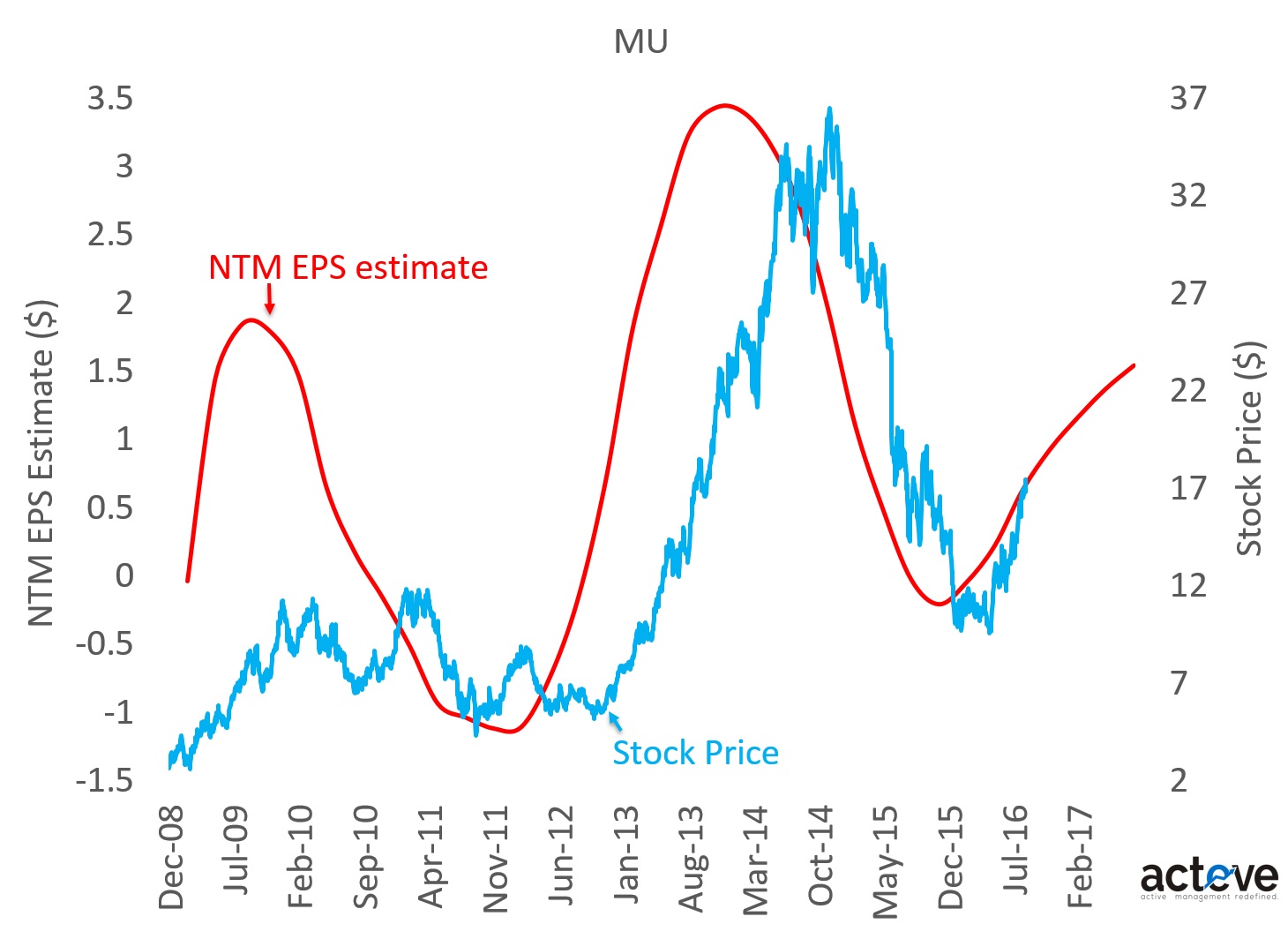

Cyclical supply/demand recovery: A combination of supply cuts and demand upgrades has pushed the memory industry into a favorable supply/demand environment, which is driving DRAM and NAND prices higher. The chart shows DRAM spot prices troughing in June and trending up through July and August. Unsurprisingly, investors have taken notice and MU stock appreciated nicely over the last two months. The chart below illustrates the correlation between MU stock price and NTM EPS estimates. The highest level of NTM EPS the Street has modeled at this point appears to be in the $1.50 range, ~50% below prior peak estimates. In other words there is plenty of room for investor imagination to be upgraded.

Technology Catch-up: Largely independent of a cyclical supply/demand tailwind, progress in 20nm DRAM and 3D NAND has been a secular reason to invest in MU. Micron’s CFO’s recent update at an investor conference indicates Micron is ahead of plans for technology advancement, and expects to have a positive report for the August quarter.

Inexpensive exposure to VR/AR and Self-Driving Car: Market participants tracking the hype cycle of VR/AR and Self-Driving Car seem to have driven up valuations for a handful of names including NVDA, AMD, and MBLY, for their premium exposure to these multi-year dynamics. Conveniently missing is an extension of the compute-driven argument to DRAM and NAND, for which Micron is a key supplier.

THIS ARTICLE IS NOT AN EQUITY RESEARCH REPORT.

Disclosure: As of this writing the acteve Model Portfolio (aMP) held a long position in MU, but no positions in AMD, NVDA or MBLY.

Additional Disclosures and Disclaimer

Stock market data provided by Sentieo.

Memory market data provided by inSpectrum.