I first introduced this “technology catch-up” thesis in late-2012, and believe it has been in play more or less since then, and will continue to remain in play for the foreseeable future. Various other events in the industry over that period made it difficult for investors to identify or appreciate this underlying phenomenon consistently. Yet in my mind it remains a key value driver for MU stock.

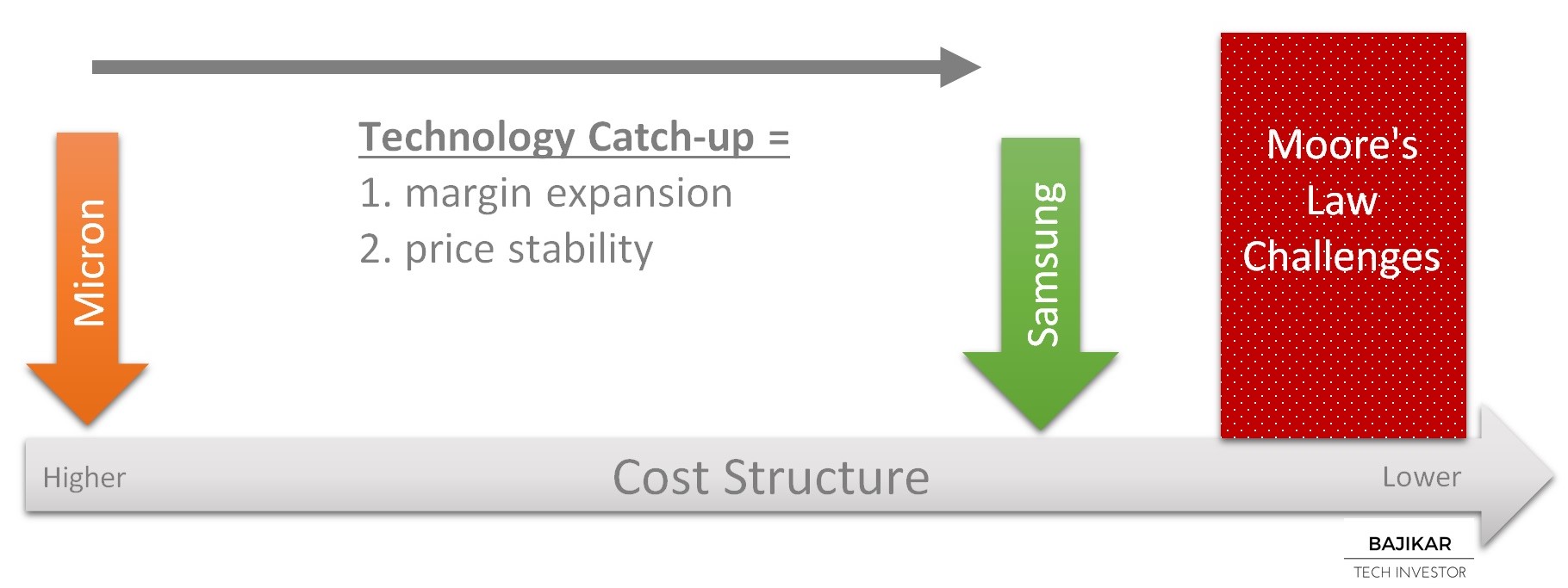

Technology catch-up means that Micron would narrow its memory cost structure gap relative to Samsung, the industry cost leader. Technology catch-up is helped by challenges involved in Moore’s Law transistor scaling such that even if scaling (aka “shrink”) is possible, it is no longer translating to commensurate cost reduction. It should be relatively obvious to see that if cost structures equalize, then Micron’s margins would close the gap relative to Samsung’s, effectively driving margin expansion for Micron. The latter part of this argument around margin expansion for Micron may however not be necessarily as obvious to some.

Here are two things to think about:

1) According to my estimates, Samsung’s memory margins have been relatively stable for the last couple of years; and market noise around Samsung being “irrational” notwithstanding, the DRAM industry overall has also generated operating margins in the ~20% range, with the industry average pulled down significantly by Micron. In other words, since ~mid-2014, Micron largely missed out on what were otherwise healthy market fundamentals, due to its chronic cost structure disadvantage.

2) In a hypothetical scenario, in a consolidated industry (3 DRAM players) with uniform cost structures, there would be virtually zero incentive for any single player to build excess capacity, or to lower prices unilaterally. It is important to recognize that this “price stability” argument breaks when cost structures diverge across industry participants. For example, the company with the lowest cost structure might find it compelling to pass through incremental cost improvements in the form of lower prices to its customers, as a recipe for taking market share while maintaining profitability – hardly evidence of irrational behavior.

To some extent there seems to be more evidence of technology catch-up in NAND, with a consensus starting to form around the prospects for 3D NAND, along with associated near-term capacity constraints and price stability. Evidence of 20nm (and/or 1Xnm) DRAM progress at Micron would bring this technology catch-up argument more in focus. Question is, as more time passes without definitive signs of 20nm product progress, does the industry argument get stronger or weaker as a value driver for MU?

THIS ARTICLE IS NOT AN EQUITY RESEARCH REPORT.

Disclosure: At the time of this writing, the acteve Model Portfolio held long positions in MU stock, but did not hold any positions in Samsung Electronics or SK hynix.

Additional Disclosures and Disclaimer

Source: DRAM and NAND Spot Price data provided by inSpectrum. Stock market data provided by Sentieo