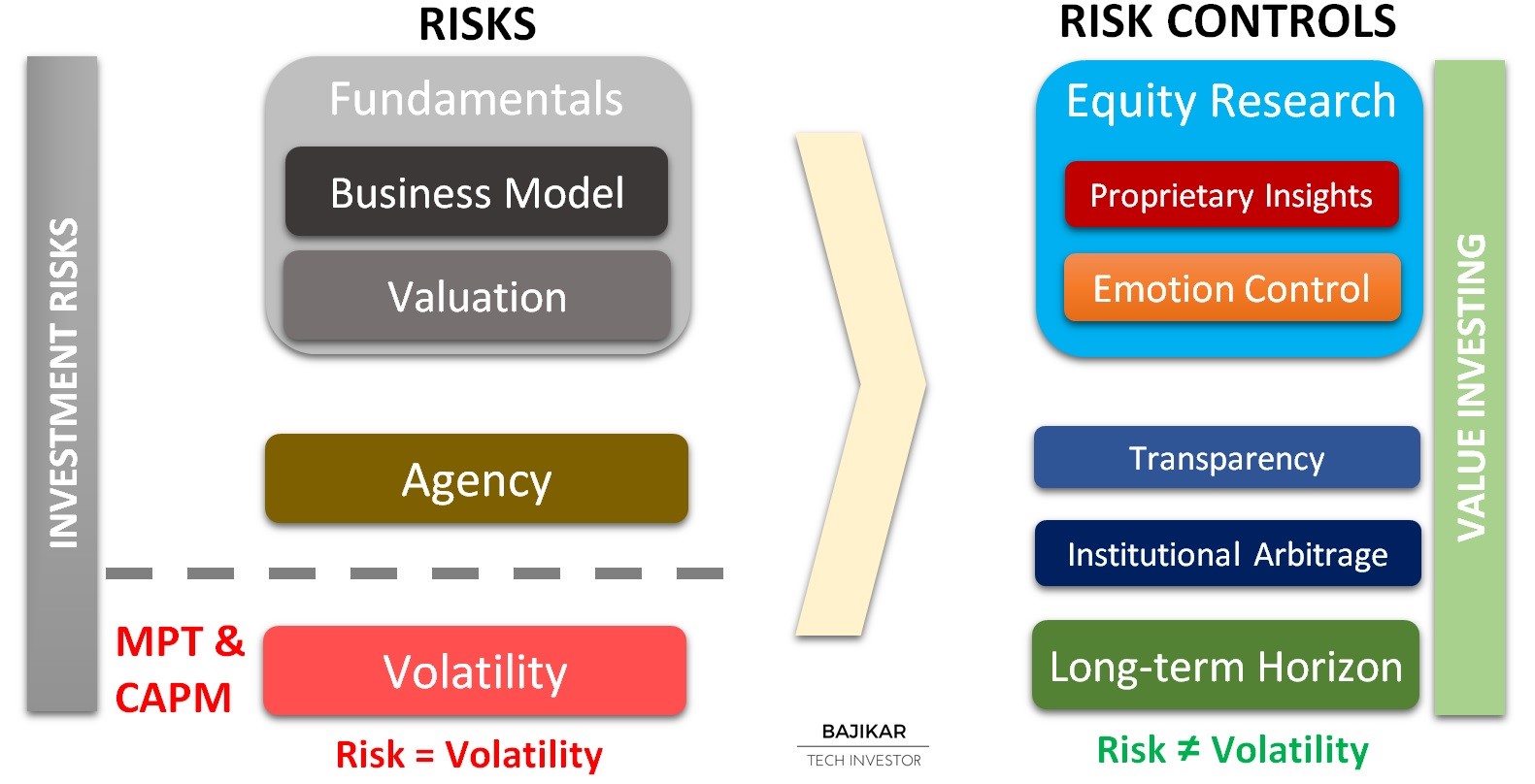

Beating the market consistently involves taking a different approach to managing investment risk. Coming up with a framework to think about different types of risks serves as a foundation for determining what risk controls to use. The chart below is one such framework that I pieced together, with help from my friend Zack Perry, who runs Vine Street Capital Management, LLC.

The chart is certainly nuanced, if not complicated, and may be a little difficult to follow for those who do not regularly analyze investments. But I do think it will help get to the core of why I believe value investing can and does deliver attractive returns while simultaneously minimizing risk.

On the left hand side of the chart is a collection of different types of risks, stacked on top of volatility, which according to Modern Portfolio Theory (MPT) and Capital Asset Pricing Model (CAPM) is the primary risk that one needs to worry about.

Fundamental risk stems from the company or assets that a stock represents. There are two parts to fundamental risk. First, you are looking for a “good” business, based on a robust definition of what “good” represents. So the risk is that your analysis is erroneous, and the business you thought was good, is not actually turning out to be that way. Second, you are looking to buy this good business at an attractive price. The risk is that for whatever reason you overpaid for the business, and this means even if the business executes like you anticipated, your investment may not generate an acceptable return. As you might guess, these issues are addressed by following a disciplined process of equity research, which mitigates the effect of mistakes driven by emotional responses.

Agency risk has to do with your ability to execute to your stated mandate as an investment manager, in the face of short-term underperformance. The risk here is that your dissatisfied clients drive up redemptions, which in turn lead to untimely liquidation of your portfolio. Untimely liquidation implies that your investments did not get a chance to live up to their full potential, and were truncated because your clients decided you were doing something wrong. Either this is because your clients never fully understood your investment approach, or because their interests have changed. This I believe is an important handicap that (large) institutional managers (e.g. mutual funds) have to work with, and represents an opportunity for (smaller) independent managers to outperform. In fact there is a term for this – Institutional Arbitrage. If you invest in stocks that institutional managers are reluctant to hold long enough primarily due to fear of redemptions, then you have a higher chance of outperformance if your thesis materializes.

Finally, there is volatility, which you will recognize as the academic definition of risk, as measured by the standard deviation of the underlying asset (stock or portfolio). The vast majority of market participants (including Robo Advisors) subscribe to this definition of risk. Within my framework, volatility provides for a relatively narrow or incomplete definition of risk, which in fact may only become relevant if one or more of the other risk elements are present. If you are investing in a company that you have researched well, paid a bargain price for, and built a client base that believes in your long-term investment philosophy, then short-term volatility becomes virtually irrelevant as an actionable element of risk. As a value investor, your goal is to take advantage of volatility (which you cannot control) to improve your entry or exit points in stocks, rather than letting volatility shake you out of your investments in an untimely fashion. That of course will be difficult to accomplish in the real world without following a disciplined process of equity research.