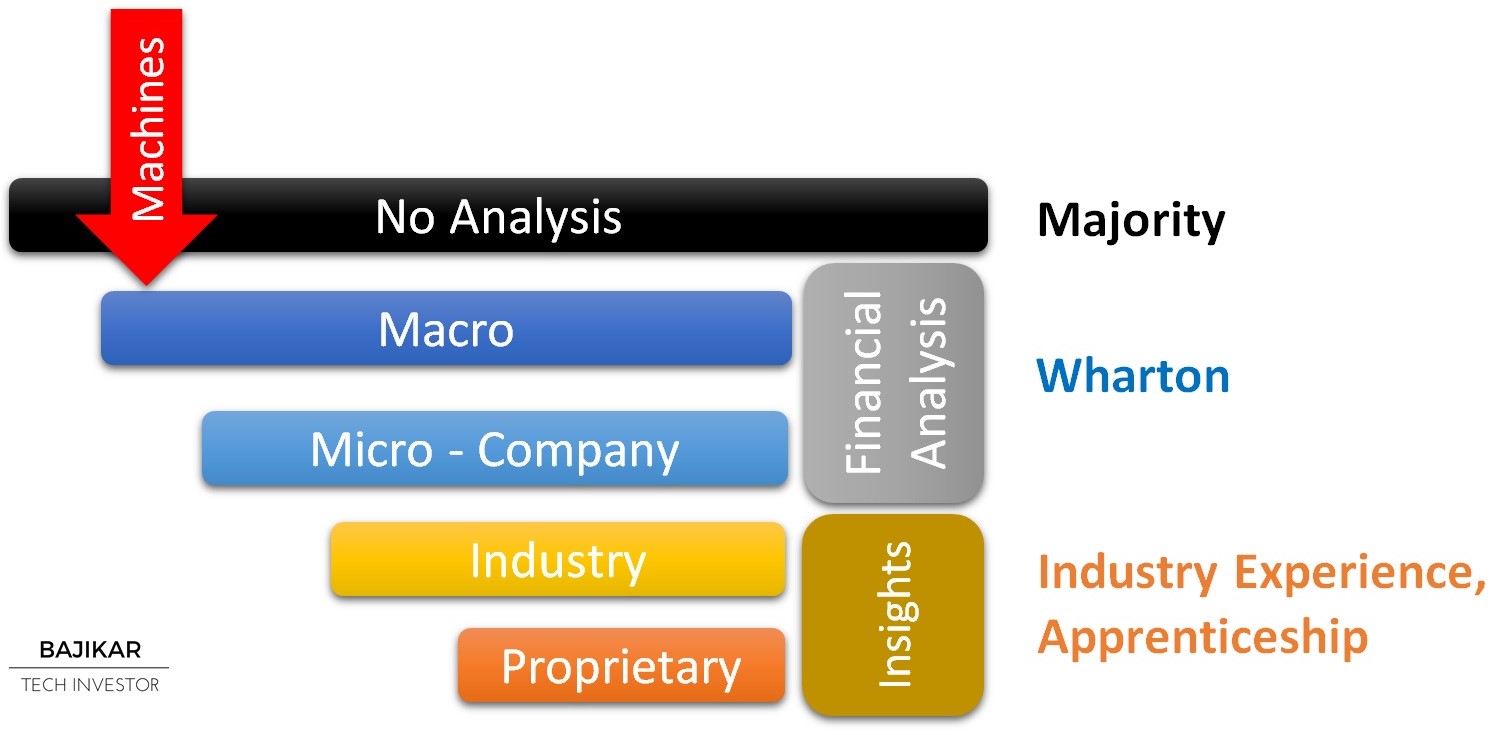

The chart illustrates my view of the difference between analysis and insight. Analysis will be the first to be commoditized with advances in machine learning, while insight continues to rule as the primary value driver for fundamental investing. As the chart suggests, analysis can be done by any qualified individual (or machine) with access to company filings. Generating proprietary insight on the other hand requires industry expertise and intuition, a scarce resource within the professional investing community. As you can probably imagine, a large number of market participants do very little or no research at all, mostly because they can get away with it. Others employ computers to extract quantitative signals from vast arrays of macro or other data. Such market participants would be the first to be disrupted by machines (e.g. Robo Advisors). That leaves a pool of investors who insist that they invest based on fundamental analysis.

Fundamental investors by definition have to claim that they “know something” that the average investor does not. However, knowing something (or hearing something), and believing what you know are importantly different things in investing. Yet behaviors that I have witnessed (see CAVM, AAPL, AMAT, IBM for example) over the years suggest investors probably do not fully understand or appreciate the difference.

Believing what you know, especially during times of stock market duress is what reinforces your investment thesis and underlying assumptions about margin of safety. This is precisely what allows you the luxury of taking advantage of general fear in the market, especially in tech stocks, where rumors and misinformation run amok. If on the other hand you find yourself ready to ditch your thesis when the market turns sour on your stock, then you should question what you really accomplished through equity research, if you bothered to do equity research in the first place.

Changing or evolving your investment thesis as new information becomes available of course is a best practice for investing success; but looking to the market price of a stock as confirmation of a change in fundamentals, is a practice that value investing seeks to avoid.

Investors hear a lot of different things, and they start to think that they know something. Reality is that they usually know little if anything without equity research, and even with equity research their knowledge is likely to be incomplete without industry expertise. So when stocks start moving against their thesis, they fret and struggle to figure out what they missed. This is not because investors aren’t smart or don’t work hard. There are a couple of issues at play here – one is of course short-term focus, which can complicate analysis. The other is lack of domain expertise.

To be clear, equity research typically isn’t an information gathering problem – it is most often a problem with inference, interpretation and intuition, i.e. with the type of information collected and with how information is processed. Investors that work hard build mountains of data, which lead to copious analysis enough to fill up an office. Yet in the tech space, such analysis doesn’t necessarily or directly translate into investment insight.

If you don’t have proprietary insights, not only do you not have an edge over other market participants, but you are also not able to build conviction around your investment thesis. Lack of confidence combined with short-term focus can and does frequently wreak havoc on investment performance. Given this, especially with fallen stocks, I often wonder if it is the companies or investors that actually destroy more value. It is just easier to blame the companies!